Unlock more financial flexibility for clients’ financial lifecycles

Using Term and Perm Life Solutions To Create A Long Term Strategy

While term life provides temporary coverage for a certain period of time to financially protect expenses like a mortgage or college tuition costs, it’s permanent insurance that provides the foundational, lifetime death benefit protection.

When the two are part of a client’s long term strategy, they can create a balanced solution that allows your client to address both their immediate and future needs. This strategy may also address potential challenges concerning coverage and budget, without having to delay the purchase of permanent life insurance protection due to its higher cost.

- A more comprehensive solution for long-term protection

- The right type of protection throughout your client’s financial life cycle

- Supplemental income: Permanent policies, like whole life, have the ability to accumulate cash value, which can be used to supplement income2

2 Access to cash values through borrowing or partial surrenders will reduce the policy’s cash value and death benefit, increase the chance the policy will lapse, and may result in a tax liability if the policy terminates before the death of the insured.

Weighing the options

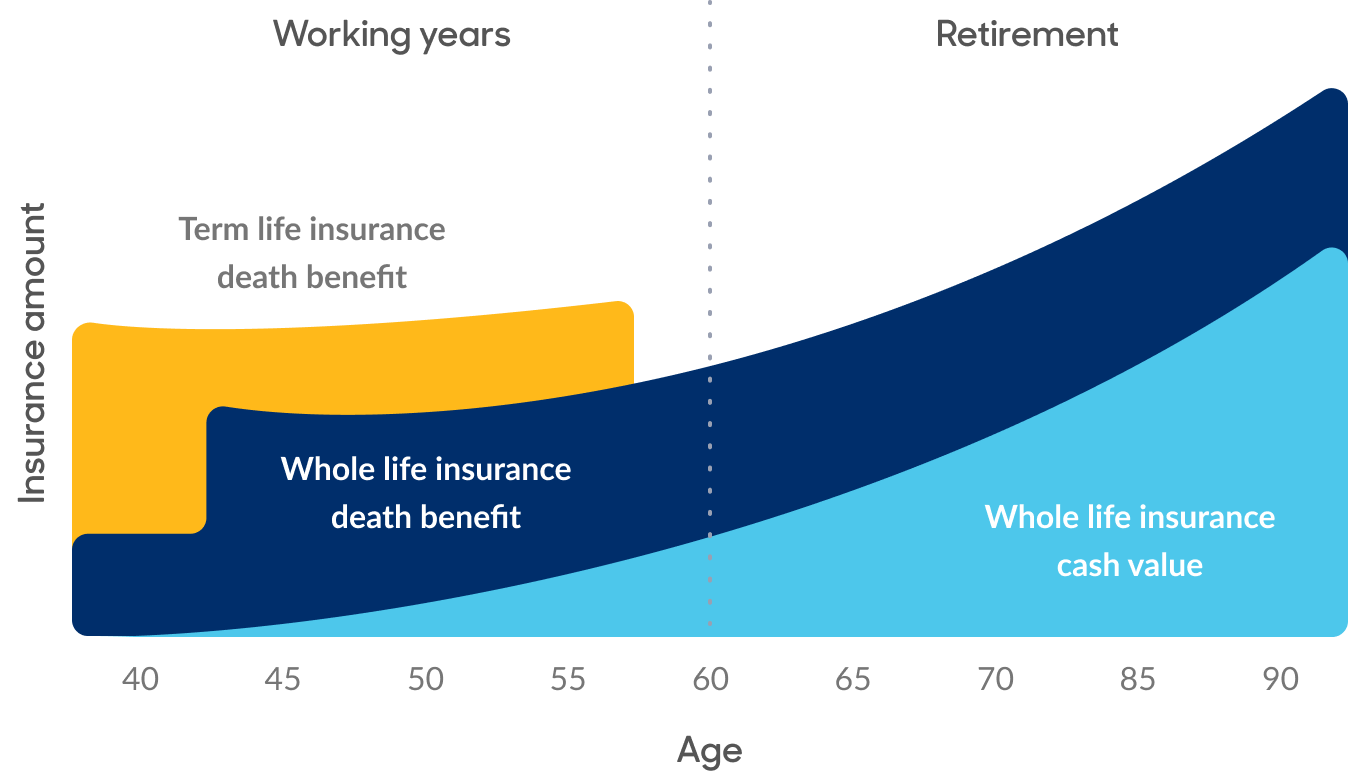

- This chart represents a hypothetical combination of term and whole life insurance, and includes the cash value pattern of whole life coverage assuming that cash value is not accessed. It is not intended to represent specific products.

- It assumes that a 20-year term life insurance policy and a participating whole life policy are purchased at age 40, and that a portion of the term life insurance is converted to whole life insurance at age 45. Guaranteed cash value will increase each year.

- Additionally, any whole life policy dividends (which are not guaranteed) that are received are used to purchase paid up additional insurance.

Click on the tabs below to explore flexible and affordable term and permanent life insurance solutions to address your client's long term protection needs.

Additional life sales campaigns:

FOR FINANCIAL PROFESSIONALS. NOT FOR USE WITH THE PUBLIC.

The information provided is not written or intended as specific tax or legal advice. MassMutual, its subsidiaries, employees and representatives are not authorized to give tax or legal advice. Individuals are encouraged to seek advice from their own tax or legal counsel.

Guarantees are based on the claims-paying ability of the issuing company and do not apply to the investment performance, or the safety of amounts held in the variable investments.

The products and/or certain features may not be available in all states. State variations will apply.

Life insurance products issued by Massachusetts Mutual Life Insurance Company (MassMutual) and its subsidiaries, C.M. Life Insurance Company (C. M. Life) and MML Bay State Life Insurance Company (MML Bay State), Springfield, MA 01111-0001. C.M. Life and MML Bay State are non-admitted in New York.

Variable universal life products are sold by prospectus. Before purchasing a variable life insurance policy, investors should carefully consider the investment objectives, risks, charges and expenses of the variable life insurance policy and its underlying investment choices. For this and other information obtain the prospectuses for the variable life insurance policy and the prospectuses (or summary prospectuses, if available) for its underlying investment choices from your registered representative. Please read the prospectuses carefully before investing or sending money.

To offer or sell MassMutual and subsidiary company variable products, producers must be a registered representative of MML Investors Services, LLC (MMLIS), Member SIPC® (www.SIPC.org), or a broker-dealer that has a selling agreement with MML Strategic Distributors, LLC (MSD). MMLIS and MSD are subsidiaries of Massachusetts Mutual Life Insurance Company (MassMutual), Springfield, MA 01111-0001, Members FINRA (www.FINRA.org).

Principle Underwriters:

MML Investor Services

MML Strategic Distributors, LLC.

©2024 Massachusetts Mutual Life Insurance Company (MassMutual®), Springfield, MA 01111-0001. All rights reserved.

Terms of Use | Privacy | MM202707-309428